Making $70,000 per year in Ontario puts you in the second tax bracket, with an average tax rate of 22.28% and a marginal tax rate of 29.65%. This means:

To break this down further:

So your total deductions are $16,278.41, leaving you with $53,721.59 in take home pay.

Ontario has one of the higher overall tax rates compared to other provinces. For example, if you made $70,000 in Alberta, your total deductions would be $14,402.34 and your take home pay would be $55,597.66.

The lowest taxes on a $70,000 income are in Nunavut, where you'd pay $11,246.79 in total tax and take home $58,753.21.

The above calculation doesn't account for any additional tax credits or deductions you might be eligible for, which would reduce your tax bill and increase your net pay.

Some credits and deductions in Ontario include:

Plugging your full financial situation into tax software will give the most accurate take home pay figure after utilizing all available credits and deductions.

Based on the after-tax income of $54,403.21 per year, your monthly take home pay on a $70k salary works out to $4,533.60.

If you're paid bi-weekly, you'll take home around $2,108.96 per paycheck, assuming 26 pay periods.

In summary, making $70,000 per year in Ontario means taking home about $54,400 after federal, provincial, CPP, and EI deductions. This results in around $4,533 per month in take home pay. Your income tax rate is 22.28% on average but climbs to 29.65% on your highest dollars earned.

For a gross annual salary of $80,000 in Ontario in 2024, the total income tax deduction is estimated to be $20,396, resulting in a net annual take home pay of $59,604, or $4,967 per month.

The average tax rate is 24.9% and the marginal tax rate is 31.5%. This means on average, 24.9% of total income is paid in taxes, while any additional income earned will be taxed at 31.5%.

Specifically, the tax brackets and rates are:

So the $80,000 salary falls within the third tax bracket, with a rate of 11.16% applied.

The total tax deduction of $20,396 is comprised of:

These mandatory payroll deductions reduce taxable income.

Additionally, voluntary Registered Retirement Savings Plan (RRSP) contributions can be deducted to lower taxable income. The maximum deduction is 18% of previous years' earned income.

Compared to other provinces, Ontario has a middle-of-the-pack tax rate on an $80,000 salary. The lowest net income is in Quebec at $56,711 after 29.1% average tax. The highest is in Nova Scotia with a net income of $56,662 after 29.2% tax.

Ontario's net income of $59,604 is higher than any Atlantic province, as well as Manitoba and Saskatchewan. It is moderately lower than Alberta and British Columbia in western Canada.

The average individual income in Ontario in 2021 was $55,300, so an $80,000 salary is 45% higher. Overall, this is considered a good above-average salary.

However, the cost of living, particularly housing, is quite high in cities like Toronto. While definitely a comfortable salary, $80,000 does not qualify as wealthy given the expenses for an individual or family.

Some key reference points for context:

So an $80,000 salary is reasonable to live comfortably by yourself or support a small family, but likely not enough to own a single-family home in Toronto.

There are a few ways to reduce taxes owed on an $80,000 salary in Ontario:

RRSP Contributions: As mentioned, contributing to an RRSP lowers taxable income. At an $80,000 income level, the tax savings from the deduction outweigh the future taxes paid on withdrawals for most people. Maximizing RRSP contributions up to the 18% deduction limit is usually advisable.

Tax-Free Savings Account (TFSA): While TFSA contributions do not reduce taxable income, investment gains and withdrawals are tax-free. This complements RRSPs nicely for retirement savings. The current 2024 TFSA limit is $6,500.

Home Office Expenses: If you work from home, even just part of the time, related expenses like office supplies and internet can be deducted. This further reduces taxable salary income.

Child Care Expenses: Paying for child care also qualifies as a deduction as long as the expenses are incurred to earn employment income. This includes daycare, nanny services, day camps during school breaks, and more.

Moving Expenses: If you have recently moved to start a new job, moving expenses can be deducted in Ontario. This includes transportation, storage, and meals during the move.

Medical Expenses: Unreimbursed medical expenses over 3% of net income can be claimed as a tax credit to reduce taxes payable. Things like dental work, prescriptions, therapy, and more count.

In summary, a gross salary of $80,000 per year results in an average take-home pay of $59,604 after 24.9% tax in Ontario. This places Ontario with moderately high taxes compared to other provinces. To reduce taxes, RRSP contributions, child care deductions, and other tax planning strategies can be utilized. While not considered a luxury salary, $80,000 provides a comfortable living in most of Ontario.

For a $65,000 annual salary in Ontario in 2023, the total income tax and payroll deductions will be about $15,703, leaving a net take home pay of $49,297 per year or $4,108 per month. The marginal tax rate is 35.6% and the average tax rate is 24.16%.

This includes $7,336 in federal tax, $3,705 in provincial tax, $3,659 in Canada Pension Plan (CPP) contributions, and $1,002 in Employment Insurance (EI) premiums.

Here is a breakdown of the major tax and payroll deductions on a $65,000 salary in Ontario:

The average take home pay on a $65,000 salary in Ontario is $49,297 per year or $4,108 per month.

This compares to a take home pay of:

So Ontario has a moderately high income tax rate compared to other Canadian provinces and territories.

Yes, $65,000 is generally considered a good salary in Ontario. It is 14% higher than the average salary in Ontario of around $57,000.

With this salary, you would have a comfortable standard of living in most areas of Ontario. However, in expensive cities like Toronto, housing costs will take up a larger portion of your take home pay.

Some key indicators on a $65,000 salary:

So in summary, $65,000 provides a comfortable life in Ontario with financial flexibility, although high costs of living in cities like Toronto present some limitations.

Ontario has one of the higher personal income tax burdens compared to other Canadian provinces.

For example, on a $65,000 salary, the total income tax in Ontario is $15,703, resulting in an average tax rate of 24.16%.

This compares to:

So a few provinces have marginally lower income taxes than Ontario, while several others are higher. But overall, Ontario ranks among the top third of provinces by tax rates.

Here are some tips to reduce income taxes and maximize your net take home pay on a $65,000 salary in Ontario:

Meeting with a tax professional can also help you create a customized plan to minimize your tax burden.

In summary, a $65,000 annual salary provides a comfortable lifestyle with financial flexibility for most individuals and families in Ontario. After deducting $15,703 in total taxes, the average Ontario resident would take home $49,297 per year or $4,108 per month.

While income taxes are moderately high compared to other provinces, Ontario residents enjoy access to high-quality public services and infrastructure funded by tax dollars. And by taking advantage of all available deductions, credits, and smart tax planning, you can maximize your net income and purchasing power.

An annual salary of $85,000 in Ontario would have the following key tax rates and take home pay:

This results in an average tax rate of 20.14% and a marginal tax rate of 29.65%. The net monthly take home pay is $5,260.

Ontario has a progressive tax system with rates ranging from 5.05% to 13.16%:

An income of $85,000 falls into the 29.65% marginal tax bracket. This means every additional dollar earned above $85,000 would be taxed at 29.65%.

The major deductions that reduce take home pay on $85,000 of income are:

CPP and EI are mandatory payroll deductions that provide retirement, disability, survivor and parental benefits.

Ontario has higher personal income taxes compared to western provinces like Alberta and B.C. but lower than eastern provinces.

For example, on $85,000 of income:

So Ontario ranks in the middle among provinces for income taxes on a salary of $85,000.

Yes, $85,000 represents a well above average salary in Ontario. Some key comparisons:

In high cost areas like Toronto or Ottawa, $85,000 would represent a moderate middle class income. In lower cost areas, it would afford an upper middle class lifestyle.

Overall, $85,000 goes a long way across most of Ontario, allowing someone to live comfortably, though not lavishly.

After taxes and deductions, take home pay on $85,000 works out to $63,122 annually or $5,260 monthly. How far does this get you in terms of lifestyle?

So $85,000 provides a comfortable middle class lifestyle with some nice extras in most of Ontario. Not an extravagant high-flying lifestyle but far from struggling.

Here are some financial planning best practices on an $85,000 household income:

Following these tips will help those earning $85,000 to effectively manage their household finances.

In summary, $85,000 represents an above average salary that affords a comfortable middle class lifestyle across Ontario. Take home pay after taxes is around $63,000. This is enough for nice housing, transportation, entertainment, modest travel, and steady savings and debt reduction. Following sound budgeting and financial planning principles allows someone earning $85,000 to achieve most financial goals and live well.

An individual earning $150,000 in Ontario would face the following tax rates in 2023:

After taking into account tax deductions and credits, the average total tax rate would be approximately 30%, meaning the take home pay would be around $105,000 annually or $8,750 per month.

Specifically, based on the 2023 tax brackets and rates in Ontario, the taxes owed on $150,000 of income would be calculated as:

So the take home pay on $150,000 in Ontario would be approximately $105,000 per year after federal and provincial income taxes.

The main tax deductions that would apply to an individual earning $150,000 in Ontario would include:

Other common deductions like child care expenses, union dues, moving expenses, and certain employment expenses could also apply depending on the individual's personal situation.

Compared to other provinces, Ontario has medium personal income tax rates:

| Province | Tax Rate on $150,000 |

|---|---|

| Alberta | 39.00% |

| British Columbia | 43.70% |

| Manitoba | 46.40% |

| New Brunswick | 53.30% |

| Newfoundland and Labrador | 51.30% |

| Nova Scotia | 54.00% |

| Ontario | 37.16% |

| Prince Edward Island | 51.37% |

| Quebec | 48.22% |

So Ontario has lower total tax rates on $150,000 of income compared to the Atlantic provinces and British Columbia, but is higher than Alberta, Saskatchewan, and Quebec.

Some reasons why Ontario's taxes are moderately high include:

On the other hand, Ontario does not have the highest top marginal tax rates compared to some eastern provinces. It also has lower retail sales taxes than B.C. and the Atlantic region.

Yes, $150,000 per year would be considered an excellent salary in Ontario. Some key points:

So in summary, $150,000 per year would provide a very comfortable lifestyle in Ontario, even after the moderately high income taxes. It puts earners well into the top income brackets provincially and federally. Individuals or households earning this level of income have high levels of discretionary spending available relative to average Ontarians.

A $45,000 annual salary in Ontario results in an average net pay of about $33,261 per year after tax, equaling $2,772 per month. This article will analyze the key details around a $45,000 salary including:

Based on the 2023 tax rates and deductions, someone earning $45,000 in Ontario would pay the following taxes and deductions:

This totals $9,027 in annual deductions, resulting in an average tax rate of 26.1% and a marginal tax rate of 32.0%.

After these deductions, the annual net take-home pay is $33,261, equaling $2,772 per month.

A take-home pay of $33,261 per year or $2,772 per month can provide a moderate standard of living in many areas of Ontario. However, those living in high cost-of-living cities like Toronto may find it more difficult to make ends meet.

Some key considerations on a take-home pay of $2,772 per month:

In summary, a $45,000 salary could provide a comfortable lifestyle in Ontario cities with lower costs of living. But budgeting diligently would be required in high expense areas like Toronto.

When comparing the $45,000 salary to the average and median incomes in Ontario:

In summary, while a $45,000 salary might be considered moderately average for individuals in Ontario, it is below the averages for households. This is an important consideration for supporting a family.

The cost of living in Ontario can vary widely depending on the city. When assessing if a $45,000 annual salary is "good money", cost of living is a key factor.

Some comparisons in major Ontario cities:

Based on these comparisons, a $45,000 annual salary goes significantly further in smaller Ontario cities like Windsor compared to Toronto. The ability to cover basic costs of living on this salary varies widely.

There are some key income tax implications to understand on an Ontario salary of $45,000, including:

Tax Brackets

The $45,000 salary falls into the 15% federal tax bracket and the 5.05% Ontario provincial tax bracket based on 2023 tax rates. No other income would be taxed at higher marginal rates.

Tax Credits

This salary level qualifies for some basic tax credits like the Canada Workers Benefit (CWB). But it does not reach thresholds for higher income credits.

Favorable Dividend Tax Treatment

At this salary level, most dividend income would face a negative tax rate after the Dividend Tax Credit. This provides incentive for dividend investing.

Progressive Tax System

Canada uses a progressive tax system meaning average tax rates increase as income rises. By staying in the lowest federal bracket, average tax rates are minimized.

A $45,000 annual salary in Ontario results in an average take-home pay of about $33,261 per year after tax deductions. This salary represents a moderate income level compared to Ontario averages. However, it may prove more difficult to cover costs of living in expensive cities like Toronto. Careful budgeting is required to manage expenses across housing, food, transportation and savings goals. While not a high income, $45,000 provides a starting point for Canadians to grow their earnings and build financial security over time through budgeting, investing, and advancing their careers whenever possible.

For an annual salary of $130,000 in Ontario, the total income tax and payroll deductions come out to around $39,000, leaving a net take-home pay of about $91,000 per year or $7,600 per month.

The average tax rate is around 30% and the marginal tax rate is 43.41%. This means for every additional $100 earned, $43.41 would go towards taxes, leaving $56.59 in additional net take-home pay.

Here is a breakdown of the different tax rates on $130,000 per year in Ontario:

After taking all these taxes into account, the total deductions come out to about 30% of the gross $130k salary.

The major deductions from a $130k salary in Ontario include:

Total Deductions: $39,050

Net Take-Home Pay = Gross Salary - Total Deductions = $130,000 - $39,050 = $90,950 per year ($7,580 per month)

So after all taxes and deductions, the annual take-home pay on $130k in Ontario works out to approximately $91,000, or around $7,600 per month.

Ontario has moderately high personal income tax rates compared to other Canadian provinces. Alberta and Quebec for example have lower tax rates on the same $130k income:

So Alberta has the highest take-home pay due to lower tax rates, followed by Ontario, and then Quebec. The differences between provinces is largely due to varying provincial tax rates.

A gross salary of $130,000 places someone solidly in the upper-middle class. It is significantly higher than the average salaries in Ontario:

So an income of $130k is considered well above average, and affords an upper-middle class lifestyle in Ontario.

With roughly $7,600 per month in take-home pay at this level, a single individual or couple should be able to live comfortably, although expensive cities like Toronto would have higher costs of living to consider.

Overall though, $130k is considered an objectively good salary, and puts earners in the top 15-20% of income earners in the province. It provides the ability to save and invest, purchase real estate, afford luxuries, and live a comfortable lifestyle. Higher incomes do offer more purchasing power and financial flexibility however.

In summary, $130k represents an above-average salary that places earners firmly in the upper-middle income class in Ontario. It enables a comfortable lifestyle, with the ability to meet all needs and afford some wants. Many would consider $130k a "good" salary, but higher wages do provide greater flexibility and purchasing power.

For a gross annual income of $120,000 in Ontario, total income tax owed is estimated to be around $38,647, including federal tax, provincial tax, Canada Pension Plan (CPP) contributions, and Employment Insurance (EI) premiums. This results in an average tax rate of 32.2% and a marginal tax rate of 43.4% [[1]].

After these taxes and deductions, the annual net take-home pay would be approximately $81,353, which equals $6,779 per month.

The marginal tax rate indicates that any additional income earned will be taxed at 43.4%. For example, a $100 raise would generate $56.59 in net take-home pay after taxes [[1]].

As for bonuses, a $1,000 bonus would result in around $566 of net extra income after tax. Meanwhile, a $5,000 bonus would generate approximately $2,830 in additional net income [[1]].

Some of the most common tax deductions that can be claimed to reduce taxable income in Ontario include:

The more tax deductions that are claimed, the lower the taxable income will be. This helps minimize total income tax owed.

Comparing Ontario to other provinces, it has higher average and marginal tax rates than Alberta, British Columbia, Saskatchewan, and Quebec on a $120,000 salary. However, the take-home pay after tax in Ontario is still competitive.

For example, if the same gross $120,000 salary was earned in Alberta, the net income after tax would be approximately $86,286 per year, or $7,190 per month. So take-home pay is only about $911 higher per year in Alberta than Ontario. The tax rates are more favorable in Alberta, but there is not a massive difference on this income level [[6]].

In the Toronto area specifically, the average total salary is $62,050, so an income of $120,000 is 93.4% higher than the norm [[9]]. The average household income is Toronto is $121,200.

Given the high cost of living in Toronto, a gross salary of $120,000 translates to a decent standard of living. Based on average expenses, the monthly net take-home pay of $6,779 would sufficiently cover costs for an individual like housing, transportation, food, and entertainment in the city [[9]].

However, for larger households supporting children and multiple family members, this salary would provide less breathing room. Individual circumstances determine whether $120,000 constitutes a "good" salary.

But in summary, an income of $120,000 positions someone well above the averages for both individual and household incomes in Toronto. It provides the ability to live comfortably in the city as a single person while affording increased savings and investment opportunities.

Tax rates at both federal and provincial levels have changed over the years in Ontario. Comparing 2023 to 5 years ago in 2018, some of the key tax brackets have increased:

2023 Ontario Tax Brackets [[1]]

2018 Ontario Tax Brackets

While the lowest tax bracket has increased from $42,960 to $49,231, the top brackets have remained unchanged over the past 5 years. Overall, Ontario marginal tax rates are still considered high relative to other parts of North America.

For high income earners like those making $120,000 per year, some tax planning opportunities and savings strategies include:

Proper tax planning for high net worth individuals can lead to substantial tax savings over time. Consulting a certified accountant can reveal tailored opportunities based on your province, career, family status, investments, and other sources of income.

An annual salary of $120,000 in Ontario results in an average tax rate around 32.2% and net take-home pay of approximately $81,353. This provides a healthy income to live in expensive cities like Toronto as a single person or small family, though larger households may find it more challenging.

Tax rates in Ontario remain high compared to other jurisdictions, but have only increased slightly on the low end tax brackets over the past 5 years. Those earning $120,000 have tax planning options to shelter more income from taxes through registered accounts, income splitting, and other strategies. Understanding provincial tax rates and claims available in Ontario is important for high income professionals to minimize their total tax obligations.

A $52,000 annual salary in Ontario translates to a good middle-income salary. As of 2024, it falls under the second federal income tax bracket, between $50,197 and $100,391, taxed at 20.5%. At the provincial level, it falls under the second tax bracket between $46,226 and $92,453, taxed at 9.15%.

After accounting for federal and provincial income taxes, Canada Pension Plan (CPP) contributions, Employment Insurance (EI) premiums, and other deductions, the average Ontario resident will take home about $41,094 per year or $3,424 per month on a gross $52,000 salary.

Below we analyze the key deductions, income taxes, take-home pay, purchasing power, and how $52,000 compares to average and middle-class incomes in Ontario.

There are two main types of income tax rates in Canada's progressive tax system - marginal and average:

While a $52,000 salary falls under the 35.3% marginal tax bracket, the average tax rate is lower at 27.0% because not all income is taxed at the highest marginal rate. The first $50,197 is taxed at just 20.5% federally and 5.05% provincially.

The key deductions from a $52,000 annual salary in Ontario are:

This totals $14,043 in deductions, leaving an after-tax net income of $37,957 per year or $3,163 per month.

Based on the above deductions, the monthly take-home pay on a $52,000 annual salary in Ontario is:

This leaves $3,163 per month for living costs like housing, transportation, food, entertainment, etc. Individual circumstances and lifestyle will determine whether this provides a comfortable living standard.

While a gross income of $52,000 provides a middle-class lifestyle, inflation steadily erodes purchasing power over time.

An individual grossing $52,000 in 2024 would need to earn $56,860 in 2029 just to maintain the same purchasing power, assuming inflation averages 2% per year over that period.

So while $52,000 provides a decent middle-class lifestyle for an individual, it is low compared to average household incomes in the province.

As mentioned earlier, federal and provincial income tax rates in Canada are progressive - higher incomes are taxed at higher rates. In Ontario, the tax rates on a $52,000 salary are:

Federal:

Provincial:

This results in an average tax rate of 27.0% across federal and provincial taxes.

Lower-income Canadians can qualify for tax credits, rebates, and benefits to reduce taxes owed and supplement income []:

However, at $52,000 most credits/benefits start phasing out. An individual would need to earn below $24,000 to gain the full benefit.

The average retirement income in Ontario is about $27,000 per individual []. To maintain a $52,000 income in retirement:

Retirement readiness ultimately comes down to saving early and consistently throughout one's working life.

Given its positioning compared to average incomes and tax rates, a $52,000 salary provides a decent middle-class lifestyle in Ontario. However, it is low compared to average household incomes.

An individual earning $52,000 can afford a comfortable, albeit modest, lifestyle in Ontario. They can afford necessities, some extras like entertainment/vacation, and middle-class housing/transportation with careful budgeting.

However, saving for major goals like retirement or home ownership will require diligent long-term saving and likely dual incomes for those with families.

In summary, a $52,000 annual salary places an individual in Ontario's middle class with a 27% average tax rate and $3,163 in monthly take-home pay. It is comparable to average individual incomes but only half of average household incomes. While providing a comfortable lifestyle, hitting major financial goals will require prudent budgeting and conscious saving over time, especially for those supporting families. Tracking purchasing power and utilizing tax credits provides further financial flexibility.

Based on the provided search results, if you make $55,000 per year living in Ontario, Canada, you will be taxed $15,100 on your income. This includes:

Your total tax represents 27.5% of your income. Your marginal tax rate is 35.5%, meaning any additional income is taxed at that rate. For example, a $100 raise would generate $64.53 in net extra pay after taxes.

With $55,000 in gross salary, your average net take-home pay after taxes will be $39,900 per year or $3,325 per month. This is the amount you receive in your bank account for spending and saving.

There are several types of deductions taken off your $55,000 gross pay:

In total, $12,435 in deductions will be taken from your pay. These deductions help fund important government programs and services.

Ontario has lower income taxes compared to most other provinces. If you made $55,000 in Alberta or Saskatchewan, your total tax would be over $12,600, or over 22% of your income. On the other hand, Ontario taxes represent 27.5% of your $55,000 salary.

Quebec has slightly lower taxes at 27% of income. Provinces in eastern Canada tend to have higher taxes on a $55,000 salary, including over 18% in New Brunswick and over 29% in Newfoundland and Labrador.

So while not the lowest, Ontario does offer reasonably competitive income tax rates compared to other provinces.

Whether $55,000 represents a "good" salary depends greatly on your situation. Here is some context:

So while you can certainly get by on $55,000, it is below average for Toronto standards and may mean living with roommates and budgeting carefully.

In less expensive cities like Ottawa or Brampton, a $55,000 salary goes further. But in Canada's most expensive city, you would likely need over $70,000 to truly feel financially comfortable.

A $55,000 annual salary in Ontario, Canada provides around $39,900 in average net take-home pay after deducting $15,100 in total taxes. This includes federal, provincial, CPP, and EI deductions which help fund public services.

Ontario offers reasonably competitive tax rates compared to other provinces. While $55,000 is below the Toronto average, it can still support living there with careful budgeting and likely roommates. In less costly cities, it provides more comfortable middle-class living.

Whether $55,000 represents a "good" salary requires comparing it to your local cost of living, lifestyle expectations, and career prospects for future raises. But it can certainly provide the basics in Ontario along with some extra for savings and leisure if you live within your means.

An individual earning $48,000 per year in Ontario would fall into the 11.16% tax bracket for 2024. This means they pay 11.16% tax on every dollar earned above $98,463.

When combined with federal taxes, the total tax rate on $48,000 of income is approximately 26.5%, consisting of:

So in total, someone earning $48,000 per year will pay $12,698 in taxes.

After deducting $12,698 in total tax, the take-home pay or net income on a salary of $48,000 per year is $35,302 annually. This works out to $2,942 per month.

Here is the monthly net pay breakdown:

The main deductions from a $48,000 annual salary in Ontario are:

CPP contributions are set at 5.70% for 2024 up to a maximum pensionable earnings of $64,900. EI rates are 1.58% in 2024 on up to a maximum insurable earnings of $60,300.

In addition to tax and these payroll deductions, other common deductions could include group health insurance premiums, union dues, RRSP contributions, and child care expenses.

Compared to other provinces, the total tax rate on $48,000 of income in Ontario is moderately high. Ontario has the 5th highest total tax rate among the provinces.

Provinces with higher total tax rates on $48,000 of income are:

Provinces with lower tax rates on the same income include Alberta (21%), British Columbia (22.39%), and Saskatchewan (24.81%).

So Ontario is certainly not the highest tax jurisdiction in Canada, but is on the higher side.

Whether $48,000 represents a "good" salary really depends on individual circumstances and the local cost of living.

Some key considerations:

The cost of living in Ontario spans a huge range from small rural towns to the Toronto metro area.

Some examples:

So in high cost of living cities like Toronto and Ottawa, a $48,000 income will mean making some sacrifices and budgeting carefully. But in smaller regions with lower costs, it can support a comfortable lifestyle.

In summary, key points on a $48,000 annual salary in Ontario:

Whether or not $48,000 represents a "good" salary depends primarily on the local cost of living. In high cost cities, it will mean making some sacrifices, while in smaller towns it can provide a relatively comfortable standard of living.

The tax rates in Ontario on a $58,000 salary are as follows:

The combined federal and provincial marginal tax rate is 24.15% and the average tax rate is around 16.35% of total income. This means that total income taxes paid on a $58,000 salary in Ontario would be approximately $13,503, resulting in a net take-home pay of $44,497 annually or $3,708 per month.

The main deductions from a $58,000 gross salary in Ontario are:

In total, deductions of around $14,043 would be withheld from a $58,000 salary, leaving the above mentioned take-home pay of $44,497.

Compared to other provinces, Ontario has a middle-of-the-pack tax rate on a $58,000 salary. The combined federal and provincial marginal rate of 24.15% places Ontario 6th highest amongst the provinces.

The highest combined marginal rate is in Nova Scotia at 29.8% and the lowest is in Nunavut at 20.3%. This means someone earning $58,000 would take home $3,317 more by living in Nunavut compared to Ontario.

Some key comparisons:

So Ontario is certainly not the most tax advantageous province for a $58,000 salary but is around average and better than some eastern provinces.

Whether $58,000 represents a good salary in Ontario depends greatly on individual circumstances. But in general, $58,000 would be considered a decent middle-class income, particularly for a single individual.

Some key considerations:

In high-cost areas like Toronto or Ottawa, $58,000 provides a moderate standard of living. In lower-cost regions, it goes much further. Overall, while not a high income, $58,000 represents a solid salary to live comfortably in Ontario for most individuals and couples without children.

In summary, a $58,000 annual salary in Ontario results in around $44,497 in take-home pay after federal and provincial taxes. Tax rates are comparable to other large provinces like B.C. and Alberta.

While not a high income, $58,000 represents a decent middle-class salary in Ontario that allows a single person or childless couple to live comfortably in most cities, with the exception of Toronto where housing costs are high. It provides disposable income similar to the average annual spending needs.

So while $58,000 is not going to lead to lavish vacations or early retirement, it provides a solid standard of living in Canada's most populous province. With careful budgeting, most individuals and families can live well on this modest middle-income salary.

The Canadian tax deadline of May 1, 2023, has now passed. However, if you’ve missed the tax deadline don’t worry, you can still file your return and claim your tax refund.

In this guide, we will cover everything you need to know about filing after the tax deadline.

Can I file my taxes after the Canadian tax deadline?

Yes, filing late is better than not filing at all!

But the answer depends mainly on whether you owe taxes or not.

Every year thousands of people apply for their tax refund after the deadline has passed.

But even if you are not entitled to a refund, it is still very important that you file your documents as soon as possible. If you're late filing and don't owe taxes then you won't pay penalties — but you can still take a financial hit. The government will hang on to any refund until you file a return, and there might also be a delay in getting benefit payouts you're eligible for, such as the GST or Child Tax benefits.

I am due a refund. Will I be fined for filing late?

No, if you are due a refund, there will be no CRA penalty or fine for filing late.

If you worked in Canada in the past ten years, it is possible to claim a refund for these years.

However, it is good not to wait until the last moment because some refundable credits like the EI overpayment are limited to be claimed within 2 years after the end of the tax year.

You may be due a tax refund if you overpaid income tax, overpaid in the Canadian Pension Plan, or overpaid employer insurance.

Most working holidaymakers are entitled to claim something back – so it’s worth investigating how much you’re owed.

Even though there is no fine or penalty the sooner, you file the sooner you receive your money back in your account.

I’m not entitled to a refund. Do I have to file my tax return?

If you owe money to the CRA, you must file as soon as possible.

The CRA charges a late-filing penalty.

Although the CRA is often understanding in cases where income is not reported and it is not unusual for penalties to be waived if you voluntarily disclose previously unreported income.

It is also important to note that even if you could not pay your full balance owing on or before 1 May, it is possible to avoid the late filing penalty by paying the amount you owe before 1 September.

What if I’m self-employed?

Self-employed tax returns are due on June 15, 2023, but any balance owed is due on May 1, 2023.

What Happens if I skip a year filing taxes

If you skip a year of filing and do not owe any money to the CRA, nothing will happen. When filing, it is possible to claim back taxes for up to 10 years.

If you owe taxes to the CRA, you will be charged a late-filing penalty.

If you owe taxes and either don't file a return or don't pay, starting May 1 you'll start racking up penalty charges and daily compound interest on the unpaid amount.

The penalties start at five percent of the amount owing, plus one percent of the balance owing for each full month that the return is late — and compound daily interest is charged on the total amount due. If you file late more than once in four years, the penalties can double.

And if you don't report income twice or more within four years, you can be hit with a "repeated failure to report income" penalty. This penalty is a big one – 20 percent of the total amount of income that was earned and not reported in the most recent year.

How long does it take to process the previous year’s tax returns?

Most Canadian tax refunds are issued anywhere from two to 16 weeks depending on the type of return and when you filed it.

Of course, if the CRA is working through a backlog it will take longer for it to be processed.

How do I file a late return in Canada?

Well, you can file your tax return yourself with the Canadian Authorities.

Alternatively, if you would like help with your tax return, you should contact a tax professional.

Tax professionals will handle all the tricky tax paperwork, ensure you are fully tax compliant, and transfer your maximum refund straight to your bank account.

The average Canadian tax refund is $998 – so it’s definitely worth claiming back what you’re owed.

Can I make installment payments?

Yes, you can pay in installments. Make sure to contact the CRA and explore the various payment arrangements depending on your situation.

Generally, there are 3 ways to pay taxes owed:

Online banking: Set up CRA as a payee on your online banking bill payment service, and use your Social Insurance Number (SIN) as your account number.

CRA My Account: You can make payments directly from your bank account on a set date, and even set up installment payments.

In-person: You can always pay in person at most major banks, just bring along your remittance voucher or original remittance slip.

Choose whatever method you’re most comfortable with!

Can I cancel or waive penalties and interest?

Under certain circumstances, the CRA will consider offering relief. It’s best to acknowledge late or incorrect tax returns, or if your payment is late, as soon as possible with the CRA to see if they can offer options to ease your payment burden.

There are 3 ways you can do this:

As daunting as it can feel, remember that the CRA is on your side and there to help.

Missed the CRA Tax Deadline?

Are you feeling anxious and uncertain about missing the May 1st, 2023 tax filing deadline? If so, rest easy. It happens to the best of us!

It’s never too late to file your return.

If you’ve missed the tax deadline, we’ve got your back even if you’re running a little behind schedule. However, time is of the essence so it’s best to roll up your sleeves and get your tax forms in order as soon as possible.

Feel free to reach out to Filing Taxes at 416-479-8532. Schedule an NTR engagement appointment with us and take the first step toward proper management of your finances.

Disclaimer: The information provided on this page is intended to provide general information. The information does not consider your personal situation and is not intended to be used without consultation from accounting and financial professionals. Salman Rundhawa and Filing Taxes will not be held liable for any problems that arise from the usage of the information provided on this page.

T4 vs T4A – What’s the Confusion?

There is a common confusion each year among business owners as to when to issue a T4 vs T4A. Business owners who employ several individuals may have staff working full-time, part-time, or once-in-a-while. So, to whom do we issue a T4, and to whom a T4A? What’s the difference? How does it impact the employer and those who work for it? Let’s discuss this below.

Employee vs Subcontractor

Determining when to issue a T4 (vs T4A) requires determining whether an individual is an employee vs subcontractor. The following factors come into play to determine if an individual is an employee:

All of the factors above need to be considered, and a subjective determination needs to be made if a worker checks several of the boxes above to be categorized as an employee vs being self-employed.

If the worker is an employee, then the employer needs to follow all the rules applicable to employees in the province they are in, deduct payroll taxes, CPP, and EI, and contribute the employer’s portion of CPP and EI as well.

What does a T4 look like?

Here is what a T4 slip looks like. The Year box indicates the year in which the income was made.

The box with the Employer’s name shows the details of the employer issuing the T4 and the box with the Employee’s name and address should be addressed to the employee.

Important boxes to keep in mind:

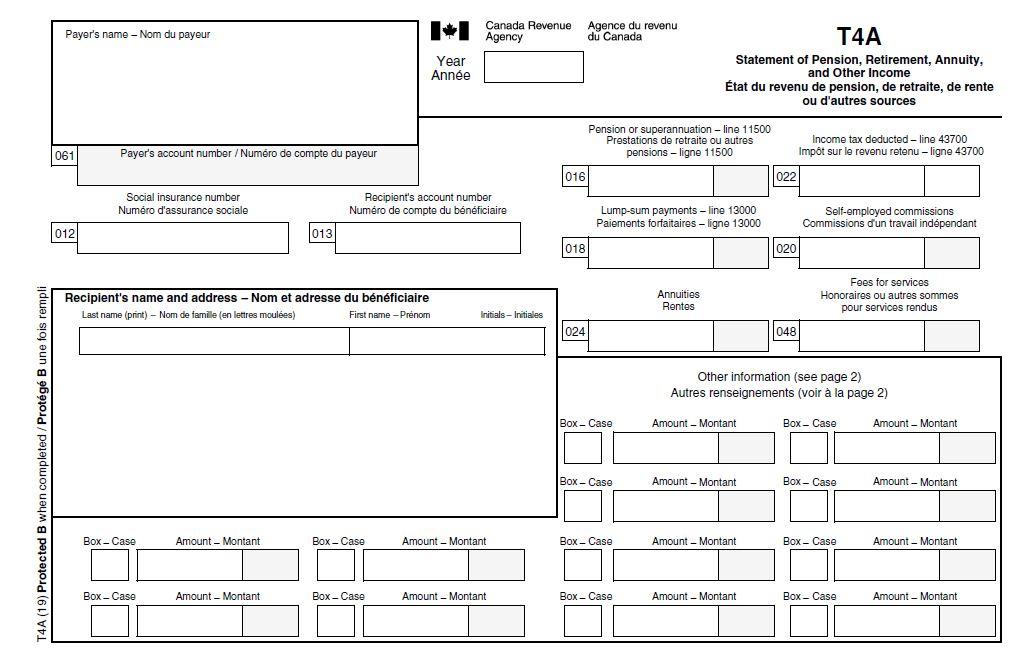

What does a T4A look like?

A T4A slip looks very similar to a T4 slip. A T4A is generally issued when the payment is made over $500. It applies in the case of self-employed commission income, pensions, annuities, fees for services, scholarships, and other income.

Similar to the T4 slip, this has the tax year, Payer’s name, and Payee’s details in the recipient’s name and address box.

Did you know?

Employers who do not issue these slips on time will be subject to fines by the CRA.

Maximize Your Tax Return

Our professionals take into account the laws in your jurisdiction, so you get the maximum benefits no matter where in the country you live. If you would like a tax accountant to file your return, book a call with our tax expert to file your taxes from start to finish. Experts at Filing Taxes will be happy to assist you in this pursuit. To speak with an experienced accountant, contact Filing Taxes either at 416-479-8532 or [email protected]. Schedule an NTR engagement appointment with us and take the first step towards proper management of your finances.

Disclaimer: The information provided on this page is intended to provide general information. The information does not consider your personal situation and is not intended to be used without consultation from accounting and financial professionals. Salman Rundhawa and Filing Taxes will not be held liable for any problems that arise from the usage of the information provided on this page.

Planning a staycation in 2022? You can claim a tax credit if you travel to Ontario this year.

Overview

The temporary Ontario Staycation Tax Credit for 2022 aims to encourage Ontario families to explore the province.

Ontario residents can claim 20% of their eligible 2022 accommodation expenses when filing their personal Income Tax and Benefit returns for 2022.

The credit will provide an estimated $270 million in support to about 1.85 million Ontario families.

Who is eligible?

You are eligible to claim the credit if you are an Ontario resident on December 31, 2022.

Only one individual per family can claim the credit for the year. Your claim can include the eligible expenses of your spouse or common-law partner and your eligible children. An eligible child is not entitled to claim the credit on their personal Income Tax and Benefit Return for 2022.

If you do not have a spouse, common-law partner, or eligible child, you can claim your eligible expenses for the credit.

Eligible expenses

You can claim the Ontario Staycation Tax Credit for accommodation expenses for a leisure stay of less than a month in Ontario, at a short-term or camping accommodation, such as a

Short-term accommodation would generally not include timeshare agreements or a stay on a boat, train, or other vehicle that can be self-propelled.

The tax credit only applies to leisure stays between January 1, 2022, and December 31, 2022, regardless of the timing of payment for the stays. The tax credit does not apply to business travel.

The accommodation expenses must also:

As long as all other conditions are met, you can claim any of the following expenses:

How to claim the credit?

You must keep your detailed receipts for any eligible expenses you incur. Those receipts should include at least all of the following information:

You can claim the credit on your personal Income Tax and Benefit Return for 2022.

The Ontario Staycation Tax Credit is a refundable personal income tax credit. This means that if you are eligible, you can get this tax credit regardless of whether you owe income tax for 2022.

Maximize Your Tax Return

Filing Taxes can help you figure out how the staycation tax credits work out in various scenarios. Our professionals take into account the laws in your jurisdiction, so you get the maximum benefits no matter where in the country you live. If you would like a tax accountant to file your return, book a call with our tax expert to file your taxes from start to finish. Experts at Filing Taxes will be happy to assist you in this pursuit. To speak with an experienced accountant, contact Filing Taxes either at 416-479-8532 or [email protected]. Schedule an NTR engagement appointment with us and take the first step towards proper management of your finances.

Disclaimer: The information provided on this page is intended to provide general information. The information does not consider your personal situation and is not intended to be used without consultation from accounting and financial professionals. Salman Rundhawa and Filing Taxes will not be held liable for any problems that arise from the usage of the information provided on this page.

Capital dividends are a special type of dividend that Canadian-controlled private corporations ( CCPC ) can pay to their shareholders on a tax-free basis. The Canada Revenue Agency ( CRA ) uses the capital dividend account ( CDA ) to keep track of the capital dividends that are available to shareholders on a tax-free basis. Capital dividends were created to improve the integration in the Canadian tax system, specifically, capital gains incurred within a corporation will have a similar impact on shareholders as if the shareholders earned the capital gains at a personal level. The tax law relating to capital dividends is complex and our CPA – CA accounting firm based in Edmonton should be consulted if you need further information or wish to claim these types of dividends as we often deal with income tax-related advice to our clients. In this blog post, we will address the most common types of transactions that impact the CDA balance. Our next blog post will include information on less common transactions when tax-free capital dividends can be paid, and additional CDA considerations.

The most common way to increase the CDA balance is through the gain on the sale of capital property (stocks, land, bonds, etc.). A capital gain occurs when the proceeds received on the sale of capital property are higher than the cost of the property, taking into consideration any costs relating to the sale, such as broker and legal fees. Only 50% of a capital gain is added to the CDA balance, which represents the non-taxable portion of the gain. The other 50% of the gain is considered taxable and is included in taxable income for the year. See Year 1 in the example below.

It is important to note that, inversely, losses on the disposal of capital property can decrease the CDA balance. 50% of the capital loss is netted against the capital gain additions and can reduce the CDA balance. Losses on a capital property cannot create a negative CDA balance; rather, the non-deductible portion of the losses is accrued until there are enough non-taxable portions of the capital gains to offset the losses. See Year 2 in the example below.

For the taxable portion of the capital losses, the remaining 50% of the taxable capital loss is applied to the current year's taxable capital gains. If there are no taxable capital gains to apply the taxable capital loss to, the taxable capital losses can be carried forward for future use or carried back 3 years to set against taxable capital gains.

Sales of depreciable capital assets can be more complicated from a CDA perspective as, more often than not, the depreciable property does not increase in value and, therefore, there is normally no capital gain or loss. In those rare cases where the depreciable property does increase in value, complex rules come into play to ensure the correct capital gain versus recapture on depreciation is calculated correctly. As these issues are complex, taxpayers should consult with their tax accountant, preferably one that has a CPA (Chartered Professional Accountant) or CA (Chartered Accountant) designation. Our CPA–CA accounting firm based in Edmonton is highly experienced in income tax matters and would be pleased to assist you in these matters.

Example

For our example, please consider that the corporation is owned by a single individual shareholder, had no other activity for each year, and that the CDA balance starts at zero in Year 1.

Year 1

A stock with a cost base of $100,000 was sold for $500,000, resulting in a capital gain of $400,000. 50% of the capital gain is included in income for tax purposes, and the other 50% of the capital gain is allocated to the CDA balance. The taxable income for the year is $200,000. The closing CDA balance for the year is $200,000. The corporation can pay a $200,000 capital dividend to its shareholder without the shareholder having to pay personal taxes. In our example, the corporation does not pay a capital dividend to its shareholders in Year 1.

Year 2

Land with a cost base of $600,000 was sold for $100,000, resulting in a capital loss of $500,000. Of the $250,000 taxable loss, $200,000 would be carried back to Year 1 and the remaining $50,000 taxable capital loss would be carried forward. The other 50% of the capital loss is allocated to the CDA balance. There would be no taxable income in Year 2 and the CDA balance would be nil as losses on a capital property do not create a negative CDA balance. There is, however, $50,000 in losses accrued ($200,000 gain from Year 1 less $250,000 loss in Year 2) that needs to be offset to bring the CDA balance above nil.

Final Words

Our experienced and professional team at Filing Taxes is here to set you on the right path considering your personal business situation. Feel free to reach out to Filing Taxes at 416-479-8532. Schedule an NTR engagement appointment with us and take the first step towards proper management of your finances.

Disclaimer: The information provided on this page is intended to provide general information. The information does not consider your personal situation and is not intended to be used without consultation from accounting and financial professionals. Salman Rundhawa and Filing Taxes will not be held liable for any problems that arise from the usage of the information provided on this page.

Did you know that some of the costs you incur in connection with relocating to a new job in Canada are tax-deductible?

Moving, in general, comes with a slew of different kinds of anxieties, as well as life changes and often significant monetary expenses. But, if you’re starting a new job in a new place, can you deduct your moving expenses? If so, what can you deduct? This is what we are going to take a closer look at here.

Tax Deductible Moving Expenses: The Basics

You may be qualified for moving expenses tax deductions if you are a Canadian resident who is compelled to change residence owing to a new job or a change in employment location.

There are conditions, of course. The Income Tax Act stipulates that you must relocate at least 40 kilometres closer to your new employment or business location to be eligible for these tax deductions. This could imply relocating to a new province, or you could also be moving within the same province; the only stipulation is that your new location is at least 40 kilometres closer to your new job than your old one.

Here’s an example: Your company is opening a new office in Kitchener, but you currently live in Toronto. As the two are some 80-90 kilometers apart (depending on where in KW you choose to move to) moving to the Waterloo Region will make the most sense, and you'll be able to take advantage of the tax deductions we’ll be discussing here as they apply to you, even though both are in Ontario and often considered reasonably close to one another.

You can claim the moving expenses tax deduction whether you are a homeowner or a tenant—the claims are essentially the same if you meet the requirements. One of the mistakes many people do make is failing to understand that only relocating homeowners are entitled to tax breaks if they make an employment-related move. However, it’s the act of moving – and its many related expenses – that we are talking about here, not the home you are moving to.

What Moving Expenses are Tax Deductible When Relocating for Work?

The following are examples of tax-deductible moving expenses:

It’s worth noting here that if your employer reimburses you for some of your moving expenses, you should keep these in mind when figuring out your deductions, as you can’t claim what someone else ultimately paid!

Tax Tips for Relocating Employees

Figuring out just which moving expenses really qualify can be tricky, and no one wants to get it wrong! Here are some tips to keep in mind.

Tax Tip #1: You don’t need receipts to deduct personal vehicle and dining costs. The cost per kilometre is determined by the region or territory from which you begin your journey. For example, you can deduct 57 cents per kilometre for driving your own car to the new location if you live in Ontario.

You can also deduct $51 per day for each household member for meals consumed during the move, up to a maximum of 15 days. Every year, the CRA adjusts the standardized meal and travel expense amounts.

Tax Tip #2: Each move is considered separately. Even if it happened in the same tax year as the first move, a second move back to your previous location and employer would qualify for moving expenditure tax deductions as well.

Tax Tip #3: If you’re selling your home to move to a new job, deduct the selling costs as moving expenses rather than add them to the home’s cost for capital gains reasons. You will get a better deduction on your income tax return if you do it this way.

Tax Tip #4: The foregoing expenses are not all-inclusive. If you suspect you have extra bills and expenses that may qualify as moving expenses, talk to your accountant.

Tax Tip #5 The Canada Revenue Agency does not allow for the reimbursement of some expenses. The following are some of these limitations:

Final Words

Need more help? To help ensure that you get all the tax breaks you are entitled to while staying on the right side of the CRA, if you have moved for work, let Filing Taxes help you prepare your tax return to ensure you get everything right!

Contact us today and let’s discuss just how we can help you. Filing Taxes concisely deals with several complex issues; it is recommended that accounting, legal, or other appropriate professional advice should be sought before acting upon any of the information contained therein.

Our experienced and professional team at Filing Taxes is here to set you on the right path considering your personal business situation. Feel free to reach out to Filing Taxes at 416-479-8532. Schedule an NTR engagement appointment with us and take the first step towards proper management of your finances.

Disclaimer: The information provided on this page is intended to provide general information. The information does not consider your personal situation and is not intended to be used without consultation from accounting and financial professionals. Salman Rundhawa and Filing Taxes will not be held liable for any problems that arise from the usage of the information provided on this page.

In Canada, tax returns are always filed separately, which means that you and your partner will continue to file individual tax returns. However, if you’re using tax software, you'll have the option of “coupling” the preparation of both returns.

Filing the two individual returns together can help optimize tax returns by identifying ways in which taxes can be reduced and can help maximize the benefits for each couple.

While the process of filing your return doesn’t result in any significant changes, whether you’re married or living common-law, here’s what you need to know about filing your taxes with a partner.

The Basics

If you are newly married or in a common-law relationship, you must notify the Canada Revenue Agency of your status change. If you’re a resident of Québec, you must also notify Revenu Québec.

You're expected to communicate this change by the end of the following month after your status has changed, either through the CRA website, by phone, or by mail. For example, if you got married in June 2022, you're expected to notify the CRA and/or Revenu Québec no later than July 31, 2022.

Tax benefits for couples

It’s important to remember that when you get married or enter into a common-law relationship, the benefit amounts you’re used to receiving may change as they are calculated based on total household income. It could also mean that you become eligible for several credits or benefits you previously weren’t qualified for.

Transferring credits

If you file as a couple, you're entitled to transfer certain credits to your partner, as long as you don’t need them first. These include:

Any amounts transferred from your partner should be calculated on Schedule 2 and entered on line 32600.

Combining credits

As a couple, you're allowed to combine some of your expenses so one spouse can claim the total tax credit.

Pooled credits include:

Tips for couples

So, who is the best person to claim credit? Is that the same person that should claim deductions?

Generally, the partner with a higher income should maximize deductions to reduce paying taxes at a higher rate. On the other hand, the partner with the lowest income should claim credits like the medical expense credits, which are based on a certain dollar amount or percentage of your income.

Wrap Up

Filing Taxes Tax Experts are always here to help you figure out how tax changes will affect your return, and we look forward to helping you.

If you need any advice on tax-saving strategies from an expert tax accountant in Toronto, Mississauga, Oakville, and Hamilton feel free to reach out to Filing Taxes at 416-479-8532. Schedule an NTR engagement appointment with us and take the first step towards proper management of your finances.

Disclaimer: The information provided on this page is intended to provide general information. The information does not consider your personal situation and is not intended to be used without consultation from accounting and financial professionals. Salman Rundhawa and Filing Taxes will not be held liable for any problems that arise from the usage of the information provided on this page.

Are you a newcomer or know someone who is? As a new immigrant, your first year is undoubtedly the hardest as you are adapting to your new environment and learning new aspects of life. Filing taxes is right up there on the list of strange concepts for many – but don’t worry, that’s what we’re here for.

Newcomers are required to file an income tax return, even if they only arrived in Canada in the last few months of the calendar year.

Read this blog to learn more about Canadian taxes and the deductions and credits that are available to you.

Residency Status

As a resident of Canada, you are liable for Canadian income taxes on your worldwide income. You become a resident of Canada for income tax purposes when you establish significant residential ties in Canada. You can usually establish these ties on the date you arrive in Canada.

Significant ties include:

File a Tax Return

As a resident of Canada, you must file a tax return if you:

Even if you have not received income in the year, you have to file a tax return to continue receiving the benefits and credit payments that you are entitled to. The filing due date for personal tax returns is April 30 of the following year.

Complete Your Tax Return

There are three areas on your tax return that must be completed during preparation.

Benefits You Can Claim

Canada Child Benefit:

If you have kids, claim the Canada Child Benefit. This is a tax-free monthly benefit payment made to eligible families to help them with the cost of raising children under 18 years of age. Families with children under age 6 will receive an annual tax-free benefit of up to $6,400 per child. Those with children between the ages of 6 and 17 will receive up to $5,400 annually. Households with children with an annual income below $30,000 will receive the maximum payment.

To apply for the Canada Child Benefit, fill out and send form RC66, Canada Child Benefits Application to the Canada Revenue Agency (CRA).

GST/ HST Credit:

The GST/HST credit is a tax-free quarterly payment that helps individuals and families with low-income offset all or part of the GST/HST that they pay. You no longer have to apply for this credit, the CRA will automatically determine if you are eligible for the credit when you file your next tax return. The credit is determined by the number of children that you have registered for the Canada Child Tax Benefit or the GST/HST credit, and your family net income.

Deductions You Can Claim

RRSP Contributions:

You can deduct contributions made to a Canadian-registered retirement savings plan.

Pension Income Splitting:

If you and your partner were residents of Canada on December 31, 2015, you can elect to split your pension income. To make this election, you and your spouse or common-law partner must complete and attach Form T1032.

Moving Expenses:

Generally, you cannot deduct moving expenses. However, if you entered Canada to attend courses as a full-time student enrolled in a program at an educational institution, and received a taxable Canadian scholarship, you may be eligible to deduct your moving expenses.

Support Payments:

If you make spousal or child support payments, you may be able to deduct the amounts you paid, even if your former spouse or common-law partner does not live in Canada.

Other Deductions:

Wrap Up

Make sure you consider these tips if you are a newcomer to Canada and claim all the tax credits and deductions that are available to you. If you need any advice on tax-saving strategies from an expert tax accountant in Toronto, Mississauga, Oakville, and Hamilton feel free to reach out to Filing Taxes at 416-479-8532. Schedule an NTR engagement appointment with us and take the first step towards proper management of your finances.

Disclaimer: The information provided on this page is intended to provide general information. The information does not consider your personal situation and is not intended to be used without consultation from accounting and financial professionals. Salman Rundhawa and Filing Taxes will not be held liable for any problems that arise from the usage of the information provided on this page.

The Canada Emergency Student Benefit, or CESB, is student-centric financial relief amid the COVID-19 pandemic.

To offer financial support to post-secondary students and recent grads who lost work opportunities due to COVID-19, the government has introduced the Canada Emergency Student Benefit (CESB) a $1,250 a-month taxable benefit available for up to 24 weeks. -The Canada Emergency Student Benefit is a Government of Canada program.

This benefit is for students who do not qualify for the Canada Emergency Response Benefit (CERB) or Employment Insurance (EI).

Who Can Apply?

If you can work, you must be actively looking for work to be eligible to receive the CESB. If you still cannot find work due to COVID-19, you can re-apply for each CESB eligibility period that you are eligible for. You cannot apply for the CESB if you already applied for the CERB or EI. If you have already applied, or are receiving support from the Canada Emergency Response Benefit (CERB) or Employment Insurance (EI) you are not eligible to apply for the CESB.

Eligibility

Check the below to see if you are eligible for the CESB:

You are one of the following:

One of the following applies:

The government says students should keep records of their daily job search activities to verify they have been looking for work during the eligibility period(s) they applied for. They recommend registering with the Government of Canada Job Bank.

What are the eligibility periods?

| Eligibility period | Amount (depending on eligibility) |

| May 10 to June 6, 2020 | $1,250 or $2,000 |

| June 7 to July 4, 2020 | $1,250 or $2,000 |

| July 5 to August 1, 2020 | $1,250 or $2,000 |

| August 2 to August 29, 2020 | $1,250 or $2,000 |

Applicants can only apply for one eligibility period at a time. If their situation continues, they must re-apply for another 4-week eligibility period.

Eligibility conditions for the benefit top-up

If you meet all of the conditions above, you may also be eligible for an extra $750 every 4 weeks.

Additional support is available if at least one of the following applies:

Verifying your eligibility

The Canada Revenue Agency (CRA) will verify your eligibility to receive the CESB after you have applied. The CRA may ask you to provide supporting documents to confirm your eligibility at a later date. If we find that you are not eligible, we will contact you to make arrangements to repay any amounts you may owe.

Which periods you can apply for?

Each eligibility period is 4 weeks period with a specific start and end date. When you apply, you will receive a payment for the specific eligibility period you applied for.

You can only apply for one eligibility period at a time. If your situation continues, you must re-apply for another 4-week eligibility period.

How do students apply?

The benefit will be administered by the Canada Revenue Agency.

Students can apply through CRA My Account.

If they have not filed taxes before, they must call 1-800-959-8281 to register their Social Insurance Number (SIN) with the CRA.

They can also apply by calling 1-800-959-2019 or 1-800-959-2041 and following the instructions. They must have their SIN and eligibility periods ready.

Call the CESB general line for questions about:

Call the CRA’s general inquiries line for questions specific to your account information, including if you are:

Before you call:

To verify your identity, you’ll need your:

The government recommends students set up direct deposits through CRA My Account or through their financial institution to receive the payments sooner. They should receive a payment within 3 business days.

CESB FAQs

[sp_easyaccordion id="5203"]

If you still have unanswered questions:

These are complicated and potentially stressful times; if you have further questions, we suggest contacting the Filing Taxes team of professional accountants today at 416-479-8532. Schedule an NTR engagement appointment with us and take the first step towards proper management of your finances.

Disclaimer: The information provided on this page is intended to provide general information. The information does not consider your personal situation and is not intended to be used without consultation from accounting and financial professionals. Salman Rundhawa and Filing Taxes will not be held liable for any problems that arise from the usage of the information provided on this page.

One of the most important things to remember as a taxpayer is the deadlines for filing your taxes. The Canada Revenue Agency sets strict due dates for returns and payments. Filing your return on time helps you avoid any interest or penalties and get your refund earlier. We’ve rounded up all the major dates that matter for your taxes to make this season stress-free.

When Can I File My Taxes in 2024??

Tax Filing Deadline for Individual Tax Returns

The tax filing deadline for your 2023 tax return is April 30, 2023.

The Canada Revenue Agency usually expects individual taxpayers to submit their income tax returns by April 30 of every year. If April 30 falls on a weekend, the CRA extends the deadline to the following business day.

If you want to file early, the CRA will open its NETFILE service on February 21st to electronically receive submitted returns

Mailed responses must be received or postmarked by the due date, and electronically submitted returns must be submitted by midnight local time on the date they are due.

Tax Filing Deadline for Self-Employed Tax Returns

If you are self-employed, the CRA gives you a bit longer to submit your income tax return — you do not have to submit it until June 15, 2022. This means you are not liable for the late-filing penalty, but CRA will begin assessing interest on any unpaid amounts owing for the tax year starting May 3, 2022.

Important CRA dates and deadlines in 2024

| Date | Event |

|---|---|

| January 10 | Deadline for payment of prior year's Canada Pension Plan (CPP) contributions and Employment Insurance (EI) premiums for self-employed individuals |

| January 16 | Fourth Quarter Projected Tax Payment Due |

| January 23 | Start of Federal Tax Return Processing for 2023 |

| January 31 | Deadline for Employers to Submit W-2 Forms |

| January 31 | Distribution of Some 1099 Forms |

| February 15 | Exemption from Withholding Becomes Available |

| February 15 | Deadline for filing an extension request if you're unable to file your personal income tax return by the regular deadline |

| March 15 | Due date for filing personal income tax returns for individuals and families |

| March 15 | Deadline for payment of prior year's taxes or installments for self-employed individuals and corporations |

| April 1 | Minimum Distribution Required for Those Turning 73 in 2023 |

| April 15 | Tax Day (unless extended due to local state holiday) |

| April 30 | Deadline for filing personal income tax returns for individuals and families (regular deadline) |

| April 30 | Deadline for payment of prior year's taxes or installments for individuals and families |

| June 15 | Deadline for filing personal income tax returns for individuals and families (extended deadline) |

| June 15 | Deadline for payment of prior year's taxes or installments for individuals and families (extended deadline) |

| June 17 | Due Date for Second Quarter Estimated Taxes for 2024 |

| September 16 | Due Date for Third Quarter Estimated Taxes for 2024 |

| October 15 | Deadline for Filing Extended Tax Returns for 2023 |

| December 12 | Due date for filing T2 corporation income tax returns for the fiscal year ended June 30, 2024 |

| December 13 | Due date for fourth-quarter estimated taxes for 2024 |

| December 31 | Required Minimum Payments for Those Aged 73 and Older |

| January 15, 2025 | Deadline for Fourth Quarter Estimated Taxes for 2024 |

Tax Filing Deadline for Business Tax Returns

The CRA requires most business owners (Sole-Proprietors or Partnerships) to submit their returns by May 2, 2022, if their business fiscal year matches the calendar year. However, some businesses may opt to observe a non-calendar fiscal year, and if they do, their returns are due six months after the end of their fiscal year.

Tax Filing Deadlines for Final Tax Returns

If you are the legal representative of a deceased person, you are in charge of ensuring their final tax return is submitted to the CRA.

Again, if the deceased person or their spouse or common-law partner is self-employed, the CRA extends the due date to June 15, but it still begins assessing interest as of April 30.

GST/HST Filing Deadline

If you are a self-employed GST/HST Registrant, you will need to file a GST/HST Return regularly, even if you have no income to report. GST/HST registrants have “reporting periods” which are monthly, quarterly, or annually. Monthly and quarterly filers must file the return and payment one month after the end of the reporting period. Annual filers have until June 15 of the year following the tax year for which the return is being filed.

Deadlines for Employers

If you hire an employee, you have to have your employee complete a TD1 form within seven days of being hired. You also have to send your employee a T4 information slip by the last day of February following the year to which the information slips apply.

Finally, if you go out of business, the CRA requires you to submit your final CPP contributions, EI premiums, and income tax deductions (payroll remittances or source deductions) within seven days of closing your doors. It also requires you to submit any T4 slips as well as a T4 Summary and file it within 90 days.

Due Dates for Installment Payments

If you make installment payments throughout the year so that you can avoid a large bill at tax time, you have four due dates throughout the year. Whether you are self-employed or employed by someone else, you must submit your installment payments by March 15, June 15, September 15, and December 15 of each year.

Tracking Due Dates

To help you stay on top of filing due dates, the CRA has a mobile app. You can download it for free and set reminders for the dates that apply to you. Additionally, you can check on extensions to the usual due dates.

Final Words

If you haven’t filed your taxes in a while, get started today to avoid these potential consequences. For advice and assistance with tax planning, a CRA tax dispute, or other tax issues, get in touch with Filing Taxes today to see how we can help. Experts at Filing Taxes will be happy to assist business owners in this pursuit. To speak with an experienced accountant, contact Filing Taxes either at 416-479-8532 or [email protected]. Schedule an NTR engagement appointment with us and take the first step towards proper management of your finances.

Disclaimer: The information provided on this page is intended to provide general information. The information does not consider your personal situation and is not intended to be used without consultation from accounting and financial professionals. Salman Rundhawa and Filing Taxes will not be held liable for any problems that arise from the usage of the information provided on this page.

The Old Age Security (OAS) pension is one of three main retirement income sources for seniors in Canada. It is designed to help seniors meet their income needs in retirement.

OAS is a monthly benefit available to anyone age 65 or older.

If you happen to be a senior whose income is below a certain amount, the OAS will also include the Guaranteed Income Supplement (GIS).

As part of your retirement income with the Canada Pension Plan (CPP), it’s important to understand how much OAS you’ll receive so you can be confident you’ll have enough retirement income.

Like the Canada Pension Plan (CPP), OAS is paid out to eligible recipients once every month, with direct deposits hitting your bank account on specific dates.

Unlike the CPP, you don’t need to make any contributions during your working years to qualify for the OAS pension.

To qualify for the OAS, you must be at least 65 years of age and resident in Canada at the time when your application is approved. You must also have lived in Canada for at least 10 years.

OAS recipients who currently live abroad may qualify if they meet the age requirement and were citizens or legal residents before leaving Canada.

They must also have lived in Canada for at least 20 years since the age of 18.

If you don’t meet these requirements, you may still qualify for OAS if you lived in a country that has a social security agreement with Canada and made contributions to that country’s social security system.

You receive the full OAS pension amount if you have lived in Canada for at least 40 years since turning 18.

If you have lived in Canada for less than 40 years as an adult, you get a partial benefit based on how long you have resided in Canada.

For example, if you lived in Canada for 30 years after age 18, you get 30/40th of the maximum benefit which is equivalent to $481.87 (i.e. $642.25 x 75%).

You can increase the OAS pension amount you qualify for by delaying your first payment past age 65.

OAS pension can be deferred for up to 5 years until age 70. For every month you delay, your pension payment increases by 0.60% for a maximum increase of 36% by age 70.

The maximum monthly OAS payment in 2024 is $778.45.

This amount is revised every quarter in January, April, July, and October to account for increases in the cost of living.

For example, the OAS amount increased in the January to March 2024 quarter to reflect an increase in the Consumer Price Index (CPI).

Your OAS pension benefit is paid into your bank account on these dates in 2024:

If you haven’t yet set up a direct deposit and currently get your benefits by cheque, it may arrive on or after these dates.

Note that the Federal government is switching from cheques to direct deposit for all payments and benefits.

You can set up direct payments to a bank in Canada by calling 1-800-277-9914 or online through your My Service Canada Account.

For foreign banks, complete the foreign direct deposit enrolment form

Service Canada may automatically enroll you for OAS or send you a letter asking you to apply.

If you haven’t received notification that you are enrolled after turning 64, you can apply online through My Service Canada Account or complete the paper application (Form ISP-3550) and mail it to the nearest Service Canada Centre.

For questions about your OAS benefit, contact Service Canada at 1-800-277-9914 or TTY at 1-800-255-4786.

In some cases, Service Canada will be able to automatically enroll you for the OAS pension. In other cases, you will have to apply for the Old Age Security pension. Service Canada will inform you if you have been automatically enrolled.

In most cases, you do not have to apply to get this benefit.